Hop onto any investing forum and you are bound to come across many opinions of Paypal. I have seen viewpoints that argue that it is undervalued because its market value sits at multi-year lows, and I have seen opinions that the company is pointless and will lose to Apple Pay. Both of these views lack an understanding of the actual business.

Don’t get me wrong, there are risks (as there are with any investment), but once you dig deeper into the company and look past their legacy consumer wallet business, you will find a company that has built the financial plumbing of our modern world. A boring, free cash flow generating, financial plumbing business.

My thesis is as follows:

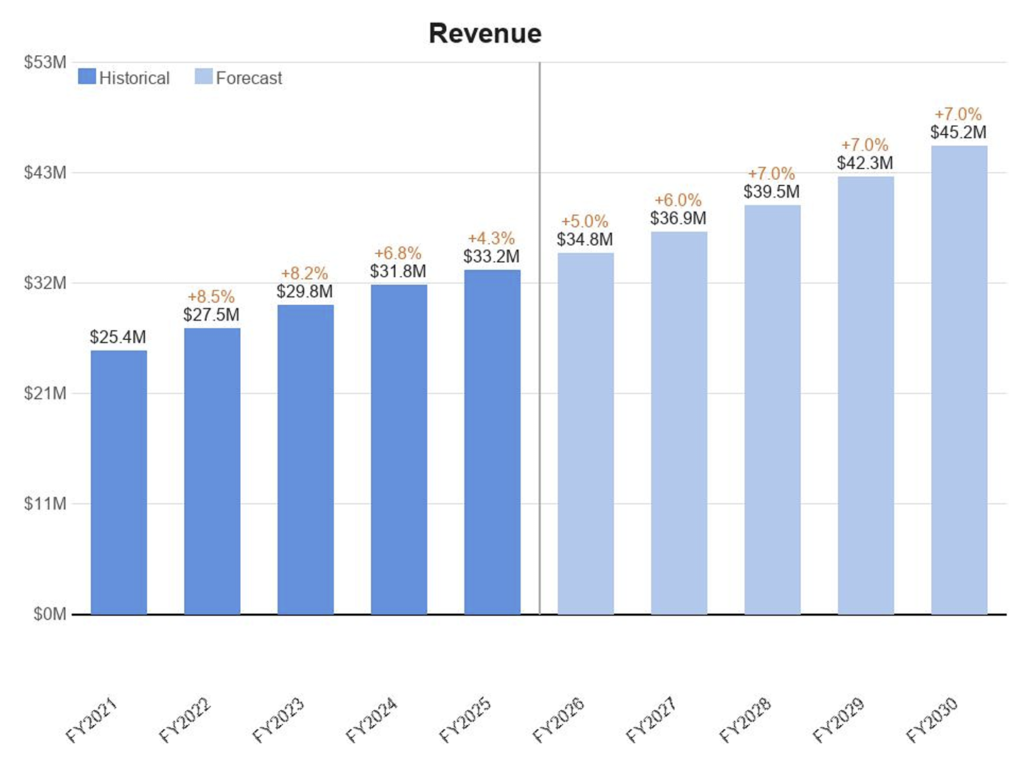

- At today’s prices, we are buying a low/mid single digit growth payments company attractively priced.

- The core business alone (branded checkout, Braintree stabilizing, Venmo base revenue) justifies an attractive IRR over 5 years and indicates an undervalued company.

- On top of this we get all of the opportunities (mentioned in the opportunities section) as growth for free. If those drivers fail to materialize to the degree forecasted in my model, the downside is protected by the core business being undervalued.

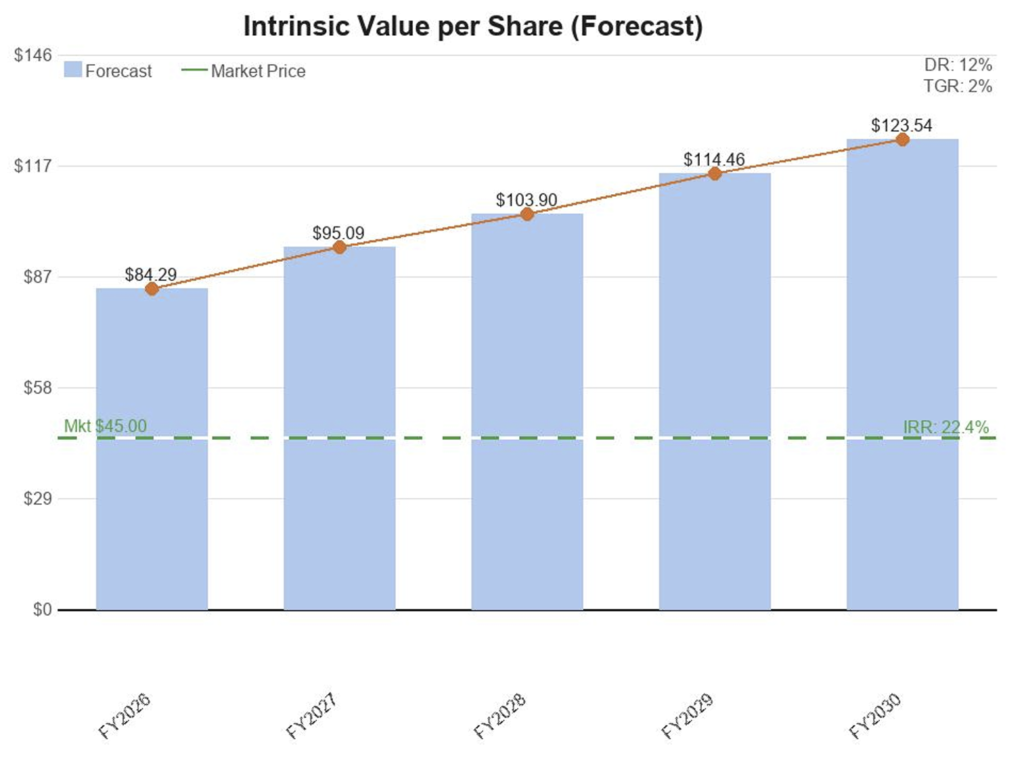

- I calculate in a base case scenario, the growth drivers contribute roughly 55% of incremental Operating Cash Flow that will drive PayPal to $8.5b in operating cashflow by FY2030 supporting a FY2026 intrinsic value of $84 and a FY2030 intrinsic value of $123.

Strengths:

Paypal has a dominant market share (47% of online payments, relative to stripe at 8% and Apple Pay at 14%) with strong brand trust backed by a two sided network of both consumers and merchants that is difficult to replicate.

Paypal is a free cash flow generating machine allowing them to buy back billions of dollars worth of their stock at very low prices (relative to intrinsic value – not just previous highs), boosting future earnings per share.

Venmo finally seems to be getting monetized via pay with Venmo. Total active accounts sit above 100 million while monetized MAUs are only 67 million. There’s still a significant chunk of the user base PayPal hasn’t converted from free P2P usage into revenue-generating commerce activity. That gap is both an opportunity and uncertainty.

An often forgotten strength is the the compliance and regulatory infrastructure. Finance is one of the most regulated industries in the world. 25 years of regulatory infrastructure (money transmitter licenses across 200 markets, KYC systems, and fraud detection at scale) creates a compliance moat that is genuinely difficult and time-consuming to replicate, and increasingly valuable as regulators tighten fintech oversight globally.

These strengths in combination with some of the listed opportunities below ssupport mid single digit revenue growth through FY2030.

Weaknesses:

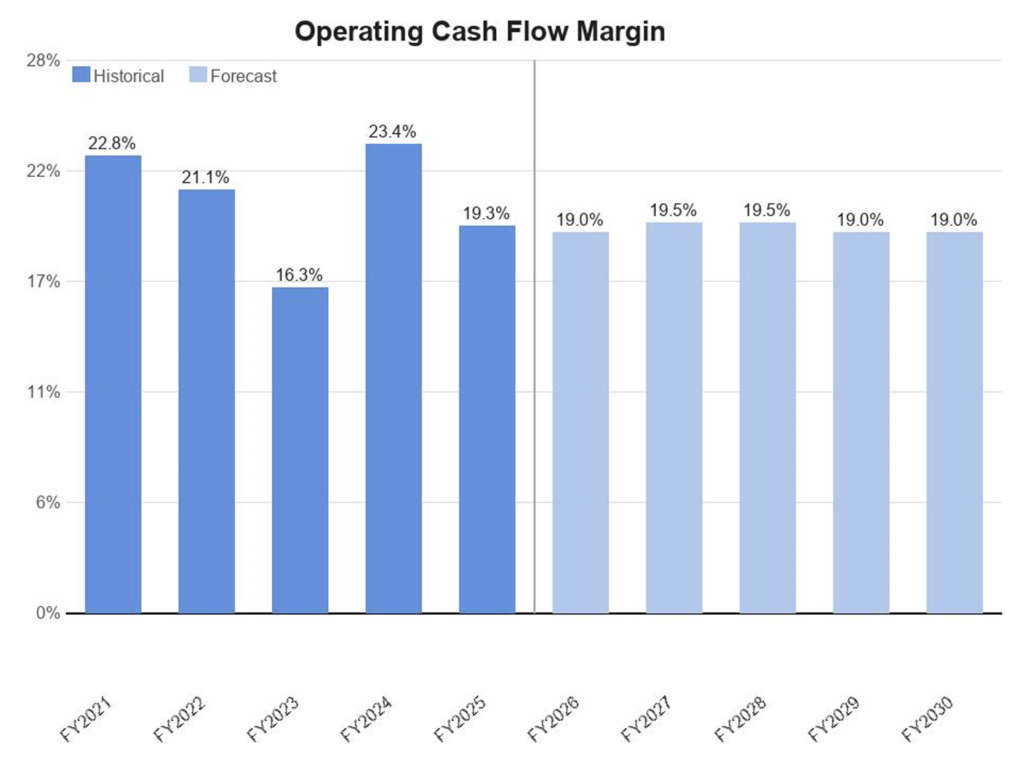

A mature and competitive market (branded checkout), with no real hardware presence, and the unbranded processing drag are weaknesses that will keep margins grounded and unlikely to break +20%.

Apple and google are baked directly into the device you have in your hand or pocket right now. Paypal requires an extra step (and although the friction has come down significantly in recent years, it is still an extra step). This will this will continue to constrain consumer-facing growth.

Brain tree (their unbranded checkout solution) is a margin drag:

- Unlike PayPal’s consumer-facing branded checkout button, Braintree operates entirely invisibly. When you pay on Uber, Spotify, Airbnb, or Adobe, you never see PayPal anywhere. Braintree is processing the transaction silently in the background and represents roughly a third of PayPal’s entire $1.8 trillion annual payment volume.

- While total payment volume grew, profits did not keep pace because the growth came from low-margin backend processing through Braintree rather than the profitable checkout button. This unbranded Braintree division faces a race to the bottom on pricing against lower-cost rivals like Stripe and Adyen.

- Branded PayPal checkout (where the consumer sees the PayPal button and trusts the brand) commands a meaningful take rate because PayPal is delivering real consumer value. Braintree is just processing infrastructure competing on price with Stripe, Adyen, and others. There’s no brand premium, no consumer loyalty, no network effect protecting margins. It’s a commodity.

- When Braintree volume grows faster than branded checkout volume, it dilutes PayPal’s overall margin even as total revenue grows. That’s exactly what happened for several years – Braintree was growing 35%+ annually while dragging overall margins lower.

- Rather than continuing to chase Braintree volume growth at any margin, PayPal deliberately slowed it down to fix the economics. PayPal’s CFO told investors the company plans to grow margin through a new pricing strategy for Braintree.

- In plain English, they stopped winning Braintree deals by undercutting on price and started requiring merchants to take value-added services alongside processing. BNPL, fraud tools, Fastlane, PayPal branded checkout options – bundled together to justify better unit economics.

PayPal’s strategy of embedding itself as processing infrastructure also drags on margins:

- It is the correct response to disintermediation, but it comes with a similar margin profile to Braintree.

- This reinforces the case for keeping OCF margin assumptions conservative rather than projecting meaningful expansion, and makes the high-margin businesses, ads, BNPL economics, Venmo, even more important to the long-term thesis

Opportunities:

Ads Manager:

Verified purchase data across 438M users creates a high-margin retail media opportunity that could materially expand transaction margins with minimal incremental cost.

- PayPal sells ads powered by purchase intent data across the open web and SMB ecosystem. Advertisers who want incremental reach beyond Amazon’s walled garden need exactly what PayPal offers.

- In the near term, ad revenue is unlikely to be material. A realistic FY2028 estimate is $100-200M as the sales organization builds. By FY2030 in a base case scenario, Using Uber Ads as a trajectory (built by the same executive now leading PayPal’s ad business, reaching $1.5B in annual revenue approximately four years from launch) a $500M run rate by FY2030 is a credible base case. (adding $300-400M in incremental OCF at high margins).

- In an upside case where the financial media network category matures faster and PayPal’s off-site data advantage gets priced by major advertisers: potentially $800m -$1B by FY2030 (contributing $600-$800m in additional OCF).

- The risk is execution. Building an ad sales organization and convincing brand advertisers to allocate meaningful budget to a new platform takes longer than the technology build. Grether has done it before at Uber, which is encouraging. But it’s the one piece of this story where patience is measured in years not quarters.

Google partnership (2025):

Integration with Google’s 2.8B users and AI commerce tools could significantly extend reach

- PayPal Enterprise Payments becomes a primary processor for transactions across Google Cloud, Google Ads, and Google Play, with PayPal’s checkout solutions including Hyperwallet and PayPal Payouts woven throughout Google’s product ecosystem.

- Both companies are working together to create “agentic commerce” – AI systems that can conduct transactions autonomously on behalf of users.

- Notably, Google has its own consumer wallet “Google Pay”. The partnership exists because PayPal and Google Pay solve fundamentally different problems. Google Pay is a consumer wallet. PayPal is global payment infrastructure with 25 years of merchant relationships, cross-border settlement capability, and enterprise processing that Google cannot replicate quickly.

Agentic commerce:

AI-driven purchasing agents need a trusted payment rail. PayPal’s AP2 protocol positions it here

- PayPal being a primary partner of Google’s Agent Payments Protocol in building the standard.

- This is potentially enormous. If AI agents become a major commerce channel, PayPal wants to be the trusted payment layer for those transactions. That’s a brand new transaction surface that didn’t exist two years ago.

BNPL expansion:

Buy Now Pay Later is growing. PayPal already has the infrastructure and customer data to compete

- The global BNPL market reached approximately $560 billion in transaction volume in 2025, marking a 13.7% year-over-year increase, with global users projected to grow from 380 million in 2024 to roughly 670 million by 2028.

- The market is projected to grow at a 23% CAGR through 2034, reaching $286 billion in provider revenue.

- PayPal BNPL segment saw a 20% volume increase, reaching over $40 billion in 2025.

- Pure-play BNPL companies like Affirm and Klarna have to hold credit risk on their balance sheets. They borrow to lend, which creates funding costs, capital requirements, and credit cycle exposure. PayPal has engineered around this entirely.

- PayPal has formalized this through agreements with KKR and Blue Owl Capital to purchase billions in BNPL receivables, meaning institutional capital funds the credit exposure while PayPal retains the fee economics and customer relationship.

- PayPal originates the loans, collects the fees, keeps the customer relationship and data, but offloads the credit risk to institutional capital partners. They get the economics of a lender without the balance sheet of one.

- PayPal Pay in 4 is accepted everywhere PayPal is (eligibility requirements and merchant opt in required). Millions of merchants including household names like Apple, Target, and Home Depot, and doesn’t even require a separate app or browser extension, just a PayPal account.

International markets:

Underpenetrated markets in LatAm, Southeast Asia, and Africa where digital payments are surging.

- They have abandoned the idea of building a competing local wallet in these markets and instead chosen a partnership model. That’s a much smarter strategy than most people realize.

- PayPal World, launched in July 2025, stitches together major global wallets like UPI, Weixin Pay, and Mercado Pago into a single interoperable platform, immediately connecting PayPal to nearly 2 billion users.

- The logic is elegant. Rather than spending a decade trying to convince a Brazilian consumer to download PayPal instead of Mercado Pago (which they’ve been using for years and trust implicitly) PayPal becomes the interoperability layer sitting above all these wallets. A merchant in the US accepting PayPal suddenly accepts Mercado Pago, UPI, and Tenpay without doing anything. A consumer in India can shop at international merchants using their existing UPI wallet. PayPal captures the cross-border transaction fee without fighting entrenched local incumbents on their home turf.

- The opportunity is not uniform across regions and the durability of PayPal’s position depends on whether they can deliver enough unique value (fraud protection, merchant trust, compliance infrastructure, agentic commerce integration) to make themselves genuinely difficult to disintermediate.

Stablecoins / crypto rails:

PYUSD stablecoin gives PayPal a foot in the door for lower-cost cross-border transactions. anyone that knows me, knows that I really dont like crypto currencies (atleast for how they are utilized in the main stream investment world). With that said… PYUSD shouldnt be viewed as a speculative crypto investment. it is quite simply financially plumbing that moves dollars on blockchain rails instead of traditional banking rails.

- Traditional cross-border payments run through the SWIFT network, a system built in the 1970s that routes money through correspondent banks, takes 3-5 business days, charges fees at multiple intermediary steps, and closes on weekends. Businesses around the world lose billions annually in cross-border fees while navigating this complex banking system.

- By enabling seamless cross-border blockchain-rail payments, PayPal is reducing transaction fees by up to 90% compared to international credit card processing, with a transaction rate of 0.99% versus the standard 2.9-3.5% plus currency conversion charges.

- It runs 24/7 and is instantaneous.

- Trust and compliance infrastructure. PayPal maintains money transmitter licenses across jurisdictions with built-in KYC verification and transaction monitoring, the regulatory groundwork that took 25 years to build. A startup trying to launch a competing stablecoin doesn’t have this. Regulators aren’t going to hand out these licenses easily in the current environment.

- PayPal processed approximately $8.2 billion in cross-border stablecoin transactions in Q1 2026 alone.

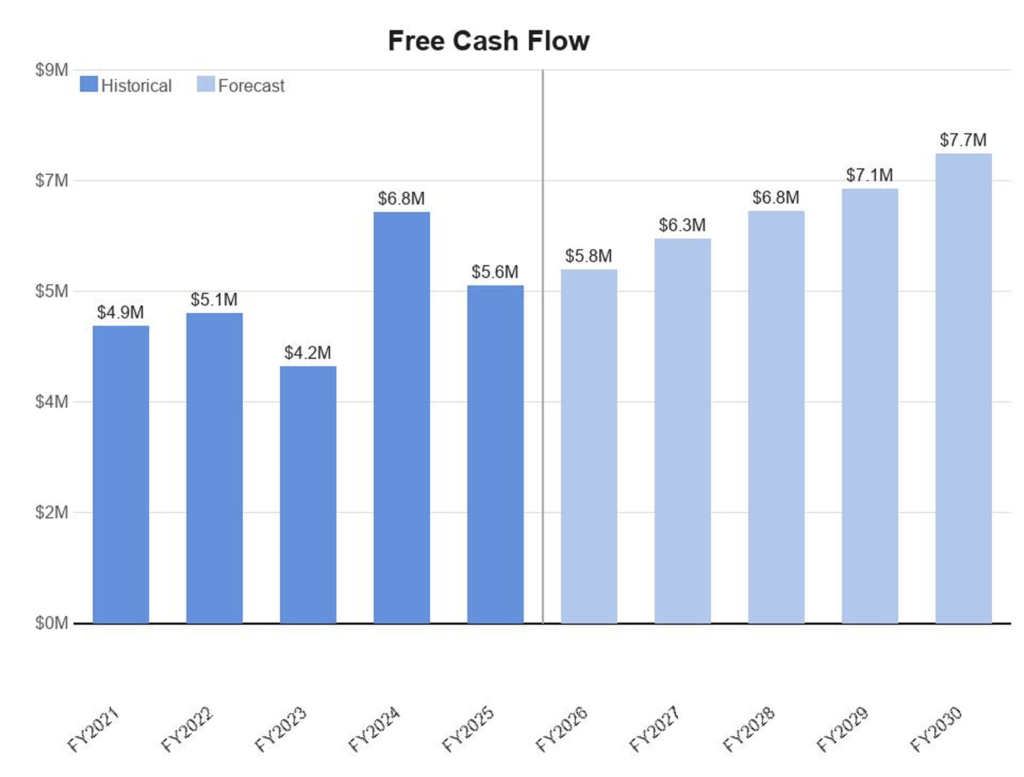

Taken together, the core business provides the floor and the opportunities provide the upside. The OCF margin chart above and the free cash flow forecast below reflect a base case that requires only moderate execution across these initiatives – not a bull case where everything goes right simultaneously.

Threats:

Apple Pay in-store dominance:

49% US mobile wallet share – as offline/online commerce blurs, PayPal’s online stronghold shrinks.

- With this said, as you can see above, Paypal and Apple Pay are two very different beasts that happen to overlap in the consumer payment processing section.

- The risk is important to understand, but PayPal doesn’t need to match Apple Pay feature-for-feature. It needs to remain the default choice for the commerce contexts Apple Pay doesn’t own. That allows them to continue building out the other sections (which will become their growth driver) of their operations.

- Apple Pay’s privacy architecture (which prevents merchant data collection and makes an advertising business structurally impossible) is the same feature that protects PayPal’s data moat. The better Apple Pay’s privacy gets, the more valuable PayPal’s verified purchase graph becomes to advertisers.

- Apple Pay is a feature. PayPal is a platform.

Regulation risk:

- Regulatory risk is real and multidimensional – covering BNPL lending standards, EU data privacy constraints on the advertising business, AI governance for underwriting models, and stablecoin licensing across multiple jurisdictions. Compliance costs are a genuine and growing margin headwind embedded in PayPal’s operating expense structure.

- However, regulation is a double-edged sword for an incumbent. PayPal has spent 25 years building compliance infrastructure (money transmitter licenses across 200 markets, KYC systems, fraud detection at scale). Every new regulatory requirement that PayPal can absorb is a barrier that prevents a well-funded startup from easily replicating their business. Regulatory tightening in BNPL specifically may accelerate the exit of weaker pure-play competitors, consolidating volume toward established players with existing compliance foundations.

Platform disintermediation – the most legitimate threat:

- Shopify (Shop Pay), Amazon, and others are building their own checkout – cutting PayPal out entirely.

- Shopify holds over 14% of the US ecommerce market and generated $11.6 billion in revenue in 2025, growing roughly 30% year over year. Every merchant on Shopify is a merchant where Shop Pay is the default, frictionless checkout option, and PayPal has to compete for attention on that same checkout page.

- With that said, PayPal has become an additional provider for processing online credit and debit card transactions for Shopify Payments in the US through PayPal Complete Payments, with PayPal wallet transactions integrated into Shopify Payments providing a consolidated view for merchants.

- The more threatening rival would be Amazon Pay. Amazon has its own closed-loop payments system, and Amazon customers rarely leave Amazon’s ecosystem to buy elsewhere. PayPal’s presence on Amazon is limited and declining. Amazon has every incentive to process payments itself and capture the economics entirely.

- PayPal’s strategic answer to the checkout disintermediation threat is Fastlane (their guest checkout solution that allows consumers to check out on any merchant’s website without a PayPal account, using stored credentials across the PayPal network). PayPal described Fastlane as “a game-changing guest checkout solution” and is expanding it to international markets.

There are risks to Paypal’s business model. What partially offsets this is threefold.

- First, PayPal is embedding itself as processing infrastructure inside these platforms rather than just competing as a button.

- Second, the open web isn’t disappearing. Enterprise merchants, B2B, cross-border, and direct-to-consumer brands still need PayPal’s global acceptance and trust infrastructure. PayPal’s Fastlane guest checkout solution (delivering 51% conversion improvements and reducing checkout from 14 clicks to 4 for early adopters) directly addresses the friction gap on the open web that Shop Pay solves within Shopify.

- Third, the diversification into Venmo, BNPL, ads, and stablecoins means PayPal’s revenue is less dependent on winning checkout specifically than it was five years ago.

Valuation and expected return:

When I factor everything into my model, it is clear to me that PayPal’s hyper growth days are over. But behind all of the fear is a boring business building the financial plumbing of our world going forward.

To reflect a business model that does contain unknowns in a market that is becoming increasingly competitive, I increased my discount rate from my standard 10% to 12%. I dont believe Paypal is a hyper growth company, so I kept my terminal growth rate set at my standard of 2%.

Today, Paypal trades at $45/share marking a 46% discount to FY2026 intrinsic value, and a staggering 63% to FY2030 intrinsic value.

If Paypal is able to successfully execute while staving off competition in their legacy business, that represents a compound annual growth rate of over 22%.

That return is driven primarily by growth in Venmo monetization, the emerging advertising platform, and BNPL expansion, with the core branded checkout business providing the floor. Even in a scenario where growth drivers underdeliver, the core business generating $6.4B in annual OCF at today’s prices provides meaningful downside protection

Whether you buy into the thesis or not, the business deserves more analytical attention than most forums give it. Do your own research, stress test the assumptions, and if PayPal fits your portfolio – remember that diversification is your friend.

**This is not financial advice – please consult your financial advisor and do your own research**