The question is not whether Artificial intelligence is valuable or not. unequivocally… it is. The question is also not whether the main beneficiaries are solid companies or not. Again for most, they are. For me, the question is simply, are those companies that have benefited from the AI buildout expensive and how can I participate further without subjugating myself to overvalued names reliant on linear 50%+ top line growth, low discount rates and high terminal growth rates just to make the expected rate of return attractive?

The price that you pay for a business will determine the value that you are able to generate from it’s operations. In my opinion, the AI beneficiaries carry too much risk (from a price perspective – not an operational one). However, there are pockets of the market that have been largely ignored due to short term issues and/or non-exciting operations that still tie back to the AI structural theme.

Enter – Northland Power:

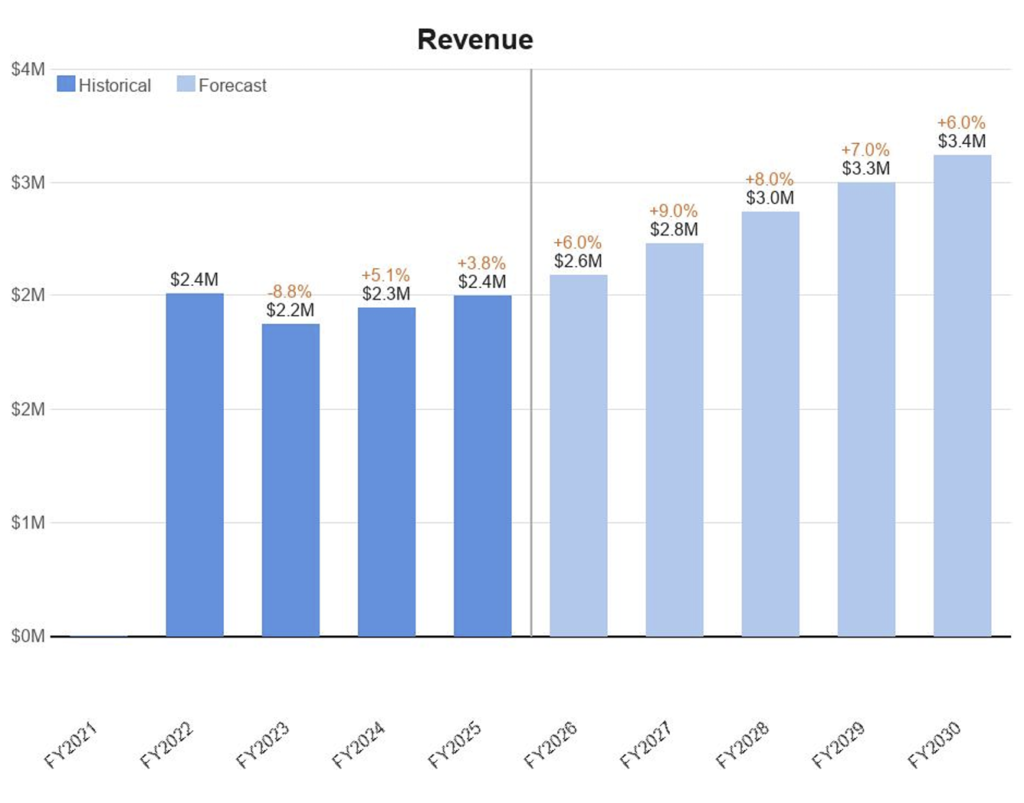

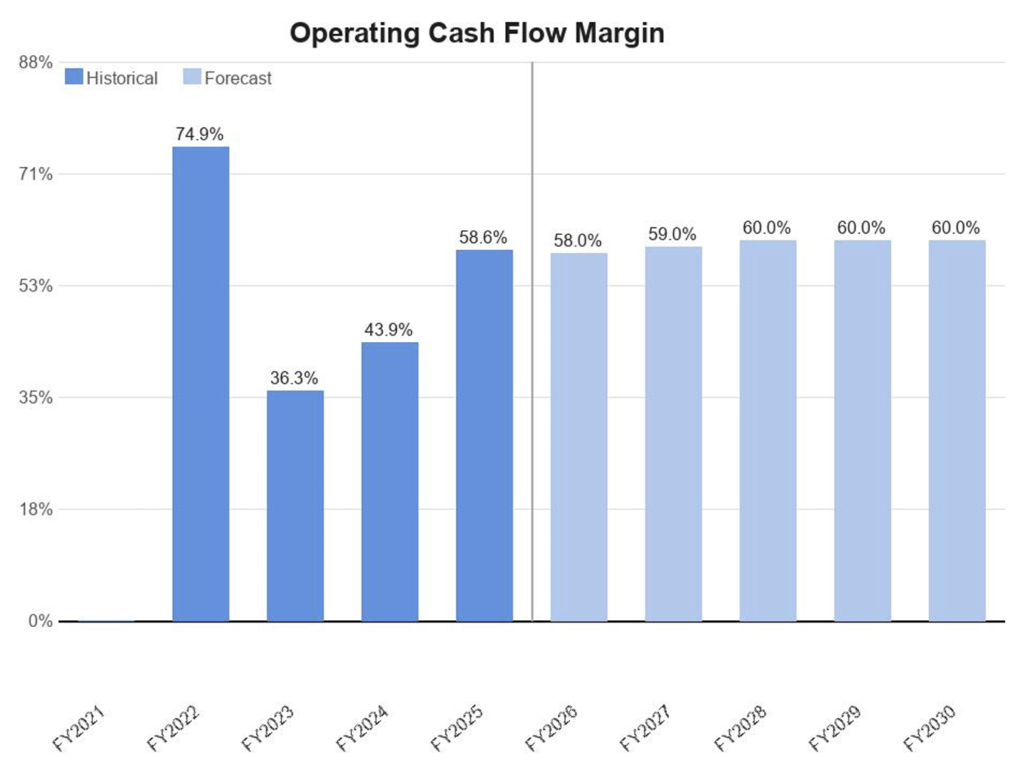

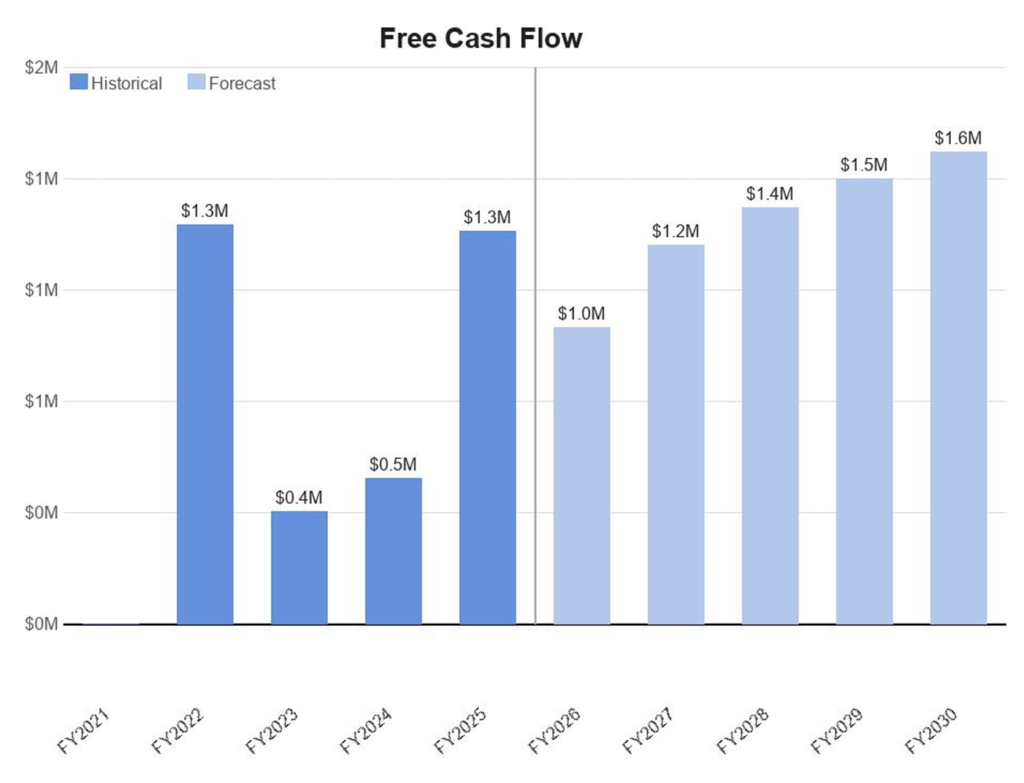

Northland Power operates wind turbine projects across the globe. Heading into 2023 on the backs of rising rates and an energy windfall they ran into some headwinds. Wind turbine projects (or any projects of this scale) require huge amounts of CAPEX, and one of the main ways of generating that capital is through the use of debt. FY2023, NPI had a debt load 8x the size of it’s operating cash flow. Higher financing costs from the increased debt position, a correction from the energy crisis of 2022, regulatory changes in Spain and Germany (creating uncertainty), as well as increased project financing costs leading to the market price re-rating over the following years. Since then, it’s been a story of higher CAPEX years compressing free cash flow as they bring on the Hai Long and Baltic power projects.

Northland Power – powering the worlds chips:

So how does Northland power take part in the AI theme? The Hai Long wind project represents a large chunk of incremental operational growth going forward and TSMC (the chip maker that fabricates 80% of the worlds advanced node chips) just signed a 30 year Power Purchase Agreement locking in that revenue stream long term. This (alongside their existing and other projects coming online) should sustain mid single digit growth (with a high single digit growth rate hump to reflect the projects ramping up in FY2027 & FY 2028) on the top line.

It’s worth noting that NPI owns about one third of the Hai Long project and their stake represents about 10% of their current and under construction projected output. The thesis is reliant not on selling energy directly to data centers or chip manufacturers, but that the use of AI has spiked demand and will continue to spike energy requirements globally. In 2025 alone, data centre electricity demand rose 17%, more than five times the 3% growth in overall global electricity demand.¹ Global data centre electricity consumption is projected to double to around 945TWh by 2030, growing at roughly 15% per year with Renewables are projected to meet nearly half of that additional demand.² Demand will remain structurally high for the foreseeable future and corporations and municipalities will be attempting to lock in as much power as possible.

The real opportunity is purchasing a company that went through largely temporary operational and financing headwinds with strong operations, a structural industry tailwind behind it, and meaningful growth opportunities ahead. For these reasons I see the operating cash flow margin stabilizing at about 60% over the medium term. TSMC signing a 30-year PPA is the trend and not the exception amongst large AI beneficiaries, and Northland is actively positioning itself to capture that demand, targeting a doubling of gross operating capacity to 7 GW by 2030. The power procurement scramble is real and in effect at Microsoft, Google, Amazon, etc. Basic economics reverberates across the entire economy leading other industries and municipalities to follow suit.

Items to Consider:

With any investment, with the good, comes the bad and Northland Power is no exception.

I mentioned the heavy debt load and although that has been moving in the right direction, it could still pose operational challenges if interest rates started to move the opposite direction.

The dividend, once hailed for its consistent growth was slashed by 40% late last year to redirect cashflow to the Baltic and Hai Long projects. I would largely view this as a positive, but sentiment was damaged by this action and may take time to recover.

Q1 2025 saw its lowest wind resource in years across European assets emphasizing the variability of a resource we can’t control. Revenue is meaningfully exposed to weather variability despite contracted pricing.

Baltic Power and Hai Long represent the two largest contributors to Northland’s capacity growth through 2027, collectively adding over 2 GW of gross capacity to an existing 3.5 GW fleet. Additionally, Geopolitical risk between China and Taiwan is worth considering in reference to the Hai Long Project specifically.

Lastly, regulation and permitting is worth a serious look. NPI walked away from a 990 MW South Korea offshore project and discontinued the High Bridge wind project in New York in Q1 2026 due to regulatory uncertainty. It’s a real and documented risk that shows the mid-stage pipeline is not guaranteed.

Despite these risks, when we balance them with the strengths and opportunities, I think that a forecast of $1.6Bn of free cash flow generated by FY2030 is both conservative and sustainable long term.

Valuation:

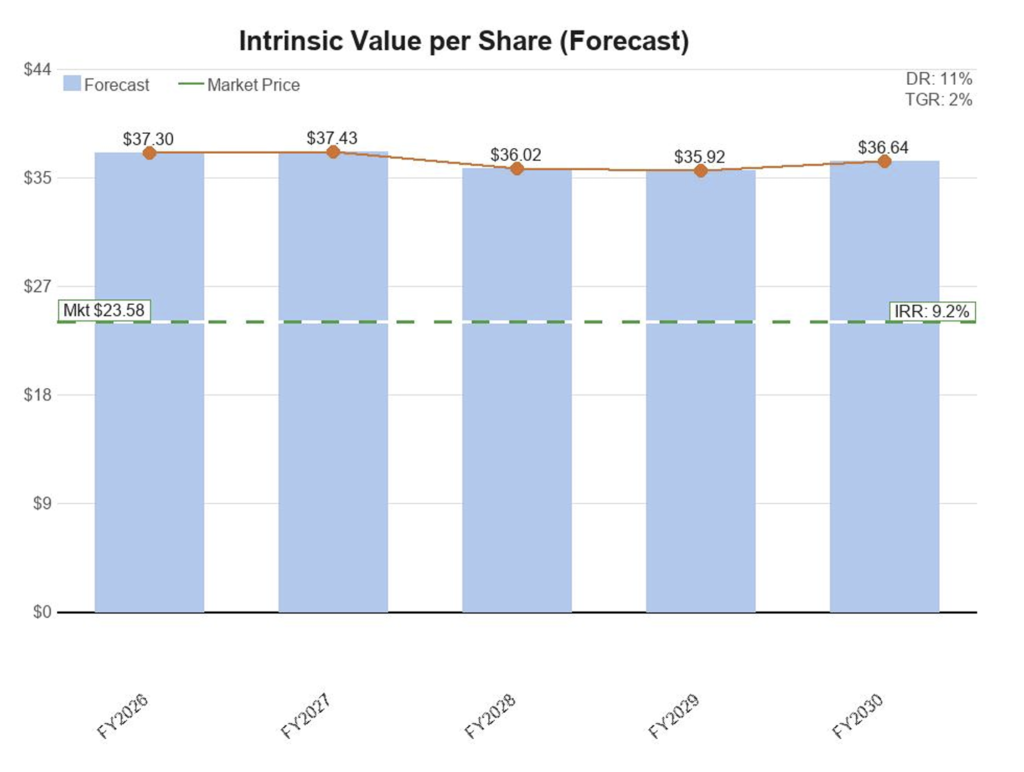

I personally believe Northland Power is a high quality company with a strong management team and deserves my standard discount rate of 10%. In light of being conservative, I utilized an 11% discount rate to reflect project and generation unknowns with a 2% terminal growth rate.

When I input my assumptions, we get the following outputs:

A stock price trading about 36% below FY2026 intrinsic value and a internal rate of return (expected return based on intrinsic value and operations) of 9.2%. add the dividend yield of roughly 3% and we get a combined RoR of just over 12% over 5 years.

These aren’t home run numbers, but to build wealth you dont need to aim for those high risk/high reward scenarios. What we have here is a high quality compounder that is likely to benefit from the increased power requirements driven by the structural AI demand theme. Rather than deciding when the memory cycle is going to normalize, or what a potential decrease in CAPEX spending from hyper scalers might do to hardware or whether the Open AI or Anthropic business model will win, you can buy a company that will continue to power the AI beneficiaries (and the rest of our economy) regardless of which direction the AI theme points.

I am a current shareholder with an average price of $17.73 and NPI is currently in my top 5 holdings. As mentioned, I personally believe NPI deserves a lower discount rate of 10% so my sell decision will likely be based on that rather than the more conservative numbers above. As NPI approaches $40 (be it over 1 year or the 5 year period) I will likely be trimming and it’s likely that I will completely sell my position if it reaches $50.

**This is not financial advice. Speak with your financial advisor and do your own research**

Foot Notes:

¹ International Energy Agency. Key Questions on Energy and AI. IEA, April 2026.

https://www.iea.org/reports/key-questions-on-energy-and-ai

² International Energy Agency. Energy and AI. IEA, April 2025.