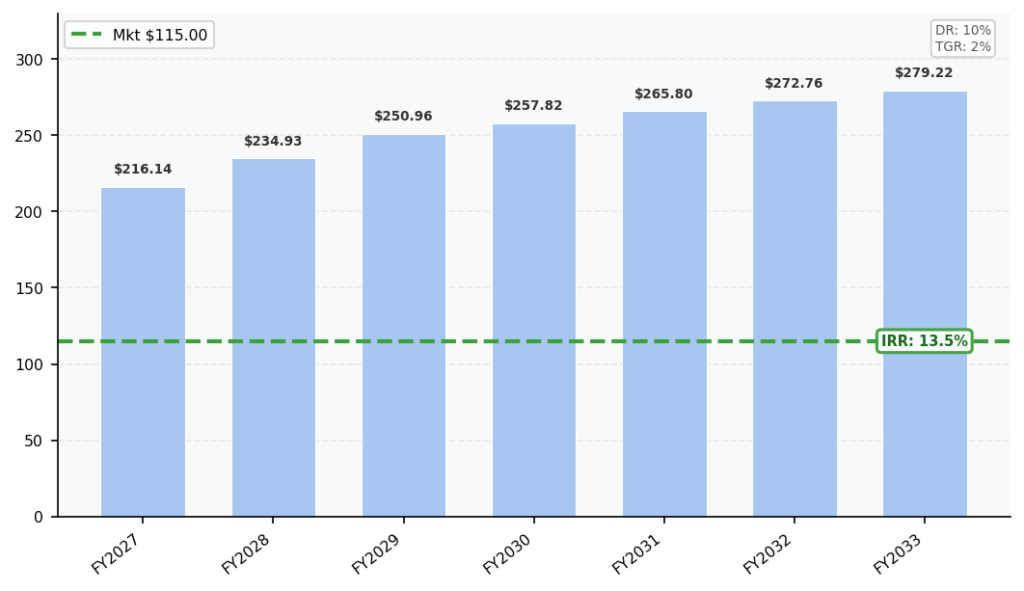

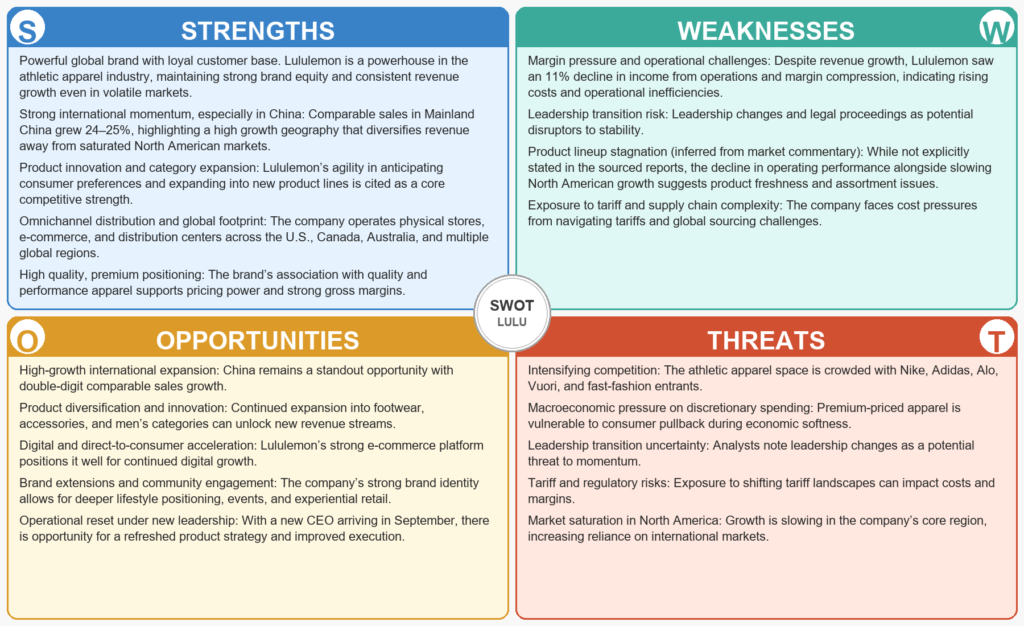

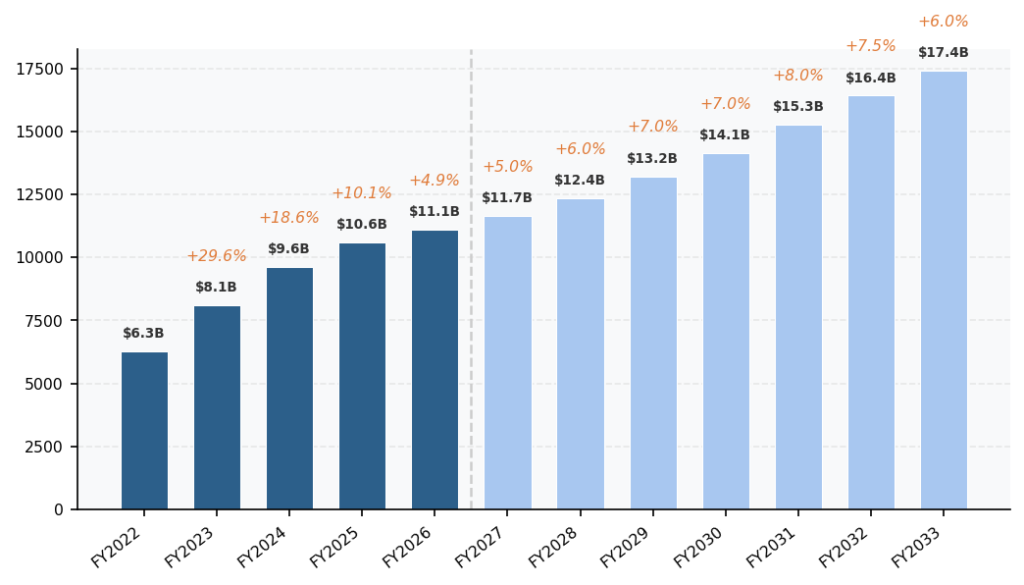

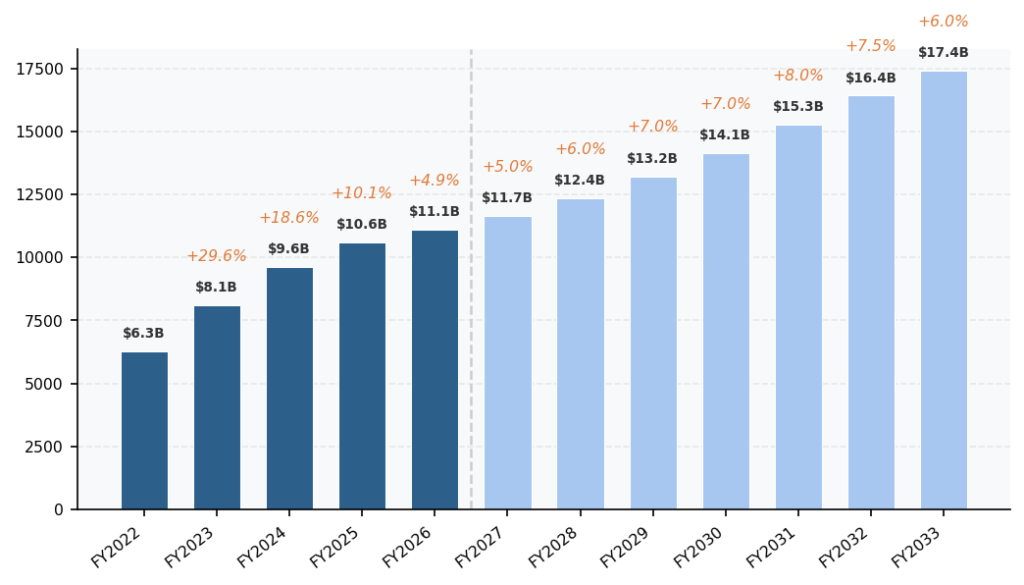

Lululemon’s recent slowdown is driven less by structural deterioration and more by a combination of U.S. market saturation and cyclical execution missteps, creating a disconnect between fundamentals and valuation. Revenue growth decelerated into FY26 as the core U.S. demographic (affluent women aged 25–45) became saturated and competition intensified. However, the drivers of margin pressure, including markdowns tied to clearing stale inventory, are temporary rather than systemic. With operating cash flow margins historically capable of reaching 18%, I am modelling stabilization at 17% and believe it credible and supported by the company’s long-term economics. The resulting FCF trajectory, rising from $1B in FY27 to over $2B by FY33 supports a valuation implying a substantial discount to intrinsic value. My DCF indicates a 40% discount to current intrinsic value and an IRR in the mid-teens under conservative assumptions using my standard 10% discount rate and 2% terminal growth rate.

Intrinsic Value:

The catalyst for unlocking this value is a product and brand reset, not a reinvention of the business model. The incoming CEO, Heidi O’Neill, is unusually well‑suited to deliver it. Lululemon’s core issue mirrors Aritzia’s 2023 slump: customers walked in and felt they already owned everything. O’Neill’s 20+ years at Nike, deep expertise in women’s sportswear, and track record scaling product engines from $9B to $45B position her as a high‑leverage operator for exactly this type of turnaround. While her September start date delays visible progress, the strategic playbook (refreshing assortments, rebuilding brand energy, and reaccelerating mid‑single‑digit growth) is both proven and achievable. If execution normalizes and the product cycle turns, this suggests the market is materially underpricing Lululemon’s long‑term cash‑generation capacity.

Lulu’s issues are not fundamental The issues stem from a stale product lineup and weakened brand energy. This is very similar to the issues Aritzia was having back in 2023. The core market (women) would walk into the store and feel like they have everything.

Based on everything I can see, Heidi O’Neill is one of the strongest possible hires Lululemon could have made, and her background aligns exactly with the above core problem. She is fundamentally a product person, not a finance‑first operator. she spent 20+ years at Nike and was deeply involved in women’s sportswear and helped grow Nike from a $9B to $45B global leader, playing a central role in product pipeline, brand voice, and consumer connection.

The delay in her start time (cant start until September due to a non compete with Nike) likely means the next few quarters will be rough, but if Lulu is able to run a similar strategy as to Artizia, I see mid/single digit growth as plausible.

Revenue Growth:

Operating Cashflow Margins:

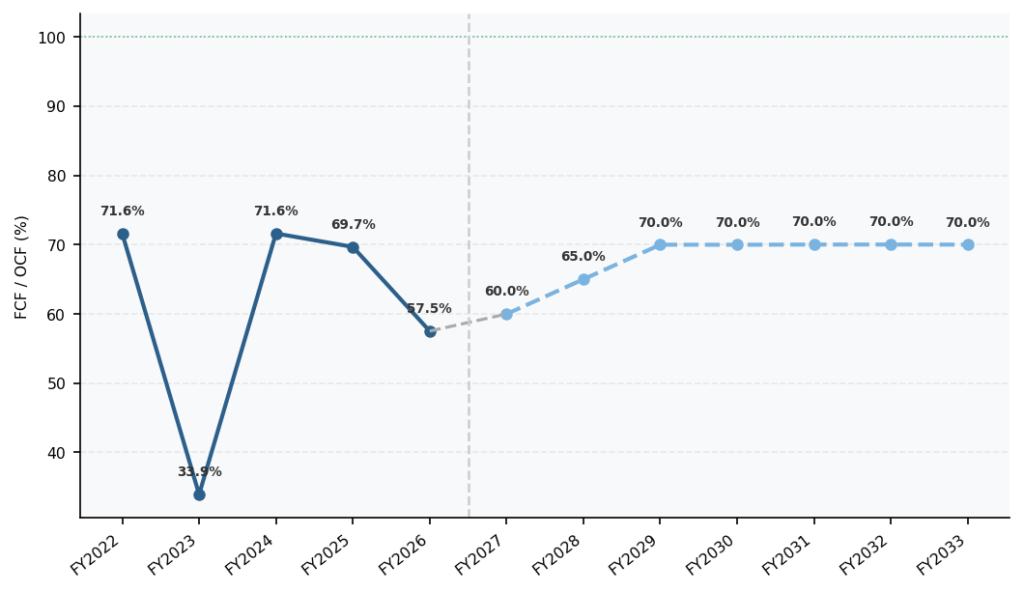

Free Cashflow Conversion (FCF/ OCF):

**This is not financial advice. Speak with your financial advisor and do your own research**