As a new dad, I have spent my fair share of time at our local Carter’s. I always assumed it was expensive, and was pleasantly surprised when I found out how reasonable the prices came out to be. My surprise continued when I pulled up their stock and saw that it was down over 60% over the last 5 years. My biggest bias is favoring companies trading at 52 week lows (and I get even more excited seeing 260 week lows)! With that said… a declining share price does not equate to a cheap stock and can more often than not point to a business in turmoil! So I broke out excel and started on my next DCF.

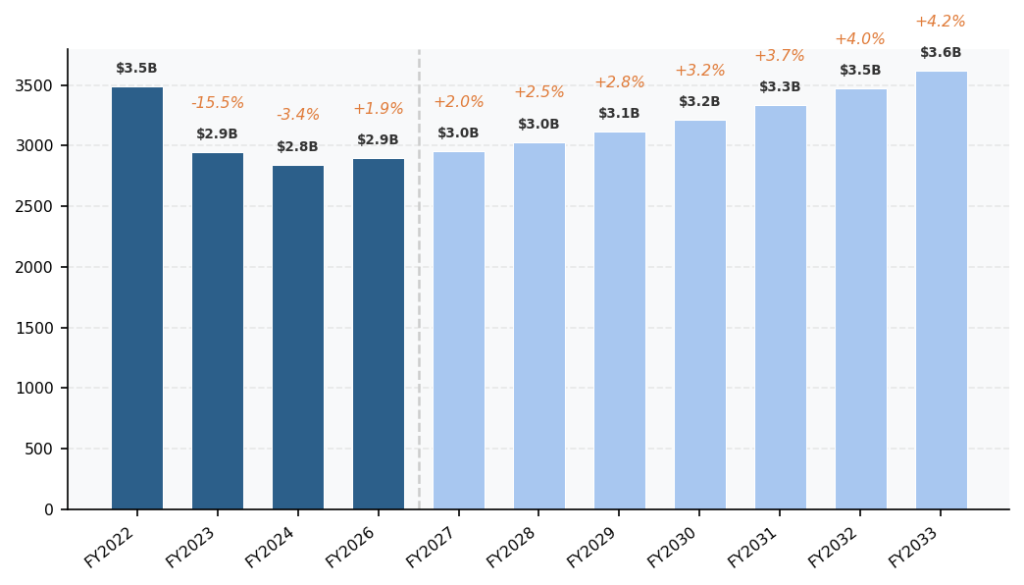

Carter’s has been in a structural decline with Revenue down to $2.9b last year from $3.5b 2021. A post covid hangover, declining birth rates, and most importantly, wholesale partners (Walmart, Target, Amazon) pulled back on orders in 2022–2024 as they worked through bloated inventories. Carter’s also carried too much product at times, leading to markdown pressure and weaker margins. This created the appearance of a business losing relevance, when in reality it was a working‑capital cycle.

Revenue Growth:

At this point I believe we are at an inflection point in the turnaround. Revenue has structurally improved due to right sized inventory level’s at Carter’s and their wholesale partners. Exclusive sub‑brands at whole sale partner’s (Child of Mine, Just One You, Simple Joys) remain category leaders. As retailers rebuild their assortments, Carter’s benefits immediately. This segment doesn’t need high growth — it just needs stability, and that’s exactly what’s returning.

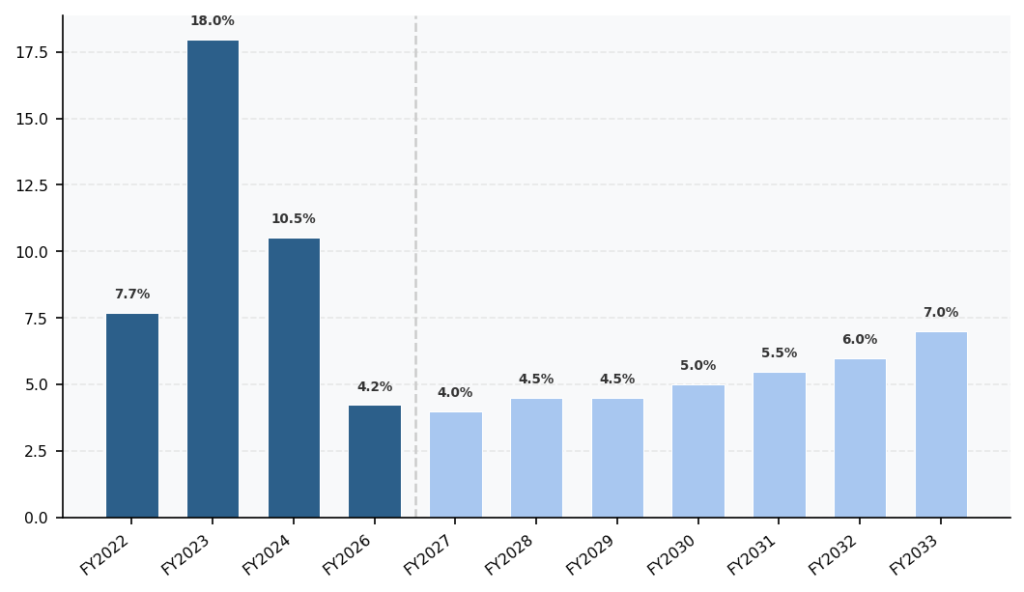

Operating Cashflow Margin:

Carter’s has been right-sizing their business. closing underperforming stores, optimizing store labour, reducing SG&A, and improved their SKU productivity all leading to operating cashflow margin’s that I believe will start to shift upwards. There are still headwinds and a shrinking demographic that will (in my opinion) prevent Carter’s from reaching previous growth and margin’s, but this isnt a growth story, its a story of stabilization and recovery.

Intrinsic Value:

There’s decent value in baby clothing:

When I use my standard Discount Rate of 10%, and a terminal growth rate of 2%, at today’s current market price of $38.20, we get a discount of 34% to FY27 intrinsic value and an IRR of over 10% to FY2033.

This is a margin of safety that I am personally comfortable with and I wouldn’t be surprised if I decide to start building a position at these levels!

As always…

**This is not financial advice. Speak with your financial advisor and do your own research**